Crocs pt 2

The Last Puff #003.5?

I wrote about Crocs in September when the price was about $77, approximately where it is today, after a round trip from $100+. I estimated CROX's intrinsic value at approx $142 per share. I’m going to give a complete fresh update in light of the information that has risen in the last 6 months, you can skip ahead if you’d like

Business

Crocs, Inc. designs, manufactures, and distributes casual footwear globally through two brands: the Crocs brand and HEYDUDE. Revenue exceeded $4 billion in FY2025. Crocs sells in 80+ countries through wholesale and direct-to-consumer channels. The company is headquartered in Broomfield, Colorado and, as of FY2025, employs roughly 6,000 people.

The business is simple enough to explain in three sentences: Crocs makes injection-molded foam footwear (primarily clogs) under its namesake brand and casual canvas shoes under HEYDUDE. The simplicity is the point. The Crocs brand generates roughly 75% of enterprise revenue and is the engine of the business. HEYDUDE, acquired for $2.5 billion in 2022, generates the remaining ~25% and is the source of essentially all controversy surrounding this stock.

The bull case on Crocs has never been about growth rates. It has been about the combination of durable brand demand, minimal capital intensity, and extraordinary cash conversion. The Crocs brand requires almost no factory ownership (Croslite resin is molded by third-party manufacturers in Vietnam), minimal R&D spend relative to revenue, and generates gross margins approaching 60%. It is, in the language of Buffett, a "tollbooth" business that collects rent on a cultural phenomenon.

Moat

The consensus view on Crocs is that it is a “fad brand” without a durable competitive advantage. This is the same thing people said in 2018 at $10, in 2020 at $20, and in 2022 at $60. The stock is up 700%+ from its 2018 lows. At some point, a “fad” that persists for two decades and generates $4 billion in revenue becomes something else.

The moat sources, ranked by durability:

1. Brand/Cultural Embedded-ness. Crocs occupies a unique position in global footwear: the intersection of comfort, customization (Jibbitz charms), and cultural irony. The brand has survived multiple death sentences from fashion critics and emerged stronger each time because consumer attachment is not driven by fashion cycle but by functional habit. Once someone owns Crocs, the repurchase rate is among the highest in casual footwear. The brand’s collaboration pipeline (Balenciaga, Post Malone, McDonald’s, Simone Rocha) keeps it culturally relevant without diluting core identity.

2. Low-Cost Manufacturing Advantage. Croslite resin is proprietary and injection-molded, not hand-assembled. A single clog can be manufactured in minutes. This gives Crocs structural gross margin advantages over cut-and-sew footwear competitors. Gross margins have consistently exceeded 55%, hitting 58.3% in FY2025 even with a 130bp tariff headwind. The manufacturing simplicity also allows rapid SKU iteration, new colors and styles can reach market in weeks rather than months.

3. DTC Mix Shift. Direct-to-consumer revenues grew 4.7% in Q4 while wholesale declined 14.5%. This is not accidental. Management is deliberately shifting mix toward higher-margin DTC, which eliminates wholesale margin capture and builds a first-party data asset. DTC now represents a growing majority of Crocs brand revenue.

4. International Runway. The Crocs brand grew international revenues at a low-double-digit rate in FY2025, with China, Japan, and Western Europe accelerating. International penetration relative to brand awareness remains early-stage in most markets. Management guides for 10% international Crocs brand growth in 2026. This is the reinvestment runway that justifies a premium. If the Crocs brand is a global category-defining product (and it is), international is a 5-7 year growth vector.

The moat is not fashion. The moat is that nobody else makes a $50 foam shoe that generates 60% gross margins, has zero fashion risk because it was never fashionable to begin with, and gets purchased repeatedly by the same consumers.

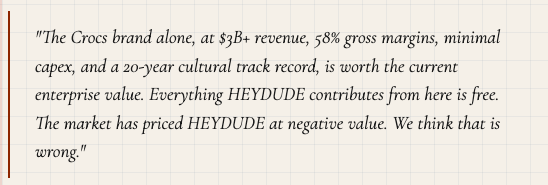

Moat Width: Medium-Wide. The Crocs brand, evaluated independently, has a durable competitive position. HEYDUDE has no moat. This distinction matters enormously for valuation, as I will discuss it later.

Management & Capital Allocation

Andrew Rees, CEO since 2017, is the architect of the Crocs brand turnaround. When he took over, Crocs was a $1 billion revenue company trading at $7 with diluted brand equity and no coherent strategy. Under Rees, the company has: simplified the product line from 300+ SKUs to a focused core, rebuilt the brand through strategic collaborations, grown revenue to $4 billion, and generated cumulative free cash flow exceeding $2 billion.

The HEYDUDE acquisition is Rees’s biggest mistake. Paying $2.5 billion (roughly 4x revenue at the time) for a brand with no moat, no proprietary manufacturing process, and declining wholesale sell-through was a capital allocation error. Management has acknowledged HEYDUDE is underperforming and has accelerated “strategic actions” (read: channel cleanup, markdown allowances, and marketing cuts). HEYDUDE revenue declined 22% YoY in Q3 2025 and is guided down mid-teens for 2026.

However, the capital return program partially redeems the HEYDUDE error:

The share count has dropped from ~63 million in early 2023 to ~50 million at year-end 2025. That is a 20% reduction in three years, funded entirely from operating cash flow with simultaneous debt reduction. At the current price and pace, Crocs is retiring ~10% of its float annually. Even if revenue is flat forever, EPS grows at high single digits from buyback alone.

Buying back 10% of your shares at 6x owner earnings is one of the highest-ROIC uses of capital available to any public company right now.

The buyback discipline is excellent. The debt paydown is excellent. The HEYDUDE acquisition was a mistake that cost shareholders real value but is being managed pragmatically, not emotionally. The $100M cost savings initiative for 2026 signals organizational seriousness.

Financial Strength & Owner Earnings

At $79.54, you are paying 6.6x owner earnings for Crocs, Inc.

For context: the S&P 500 trades at roughly 20x earnings. The footwear peer group (Nike, Deckers, Skechers, Steven Madden) trades at 15-25x. Crocs trades at 6.6x owner earnings, which is the multiple the market assigns to businesses it believes are in structural decline.

The question is whether the market is right. Is this a business in structural decline, or is this a business experiencing a temporary revenue reset driven by deliberate wholesale pullback, HEYDUDE restructuring, and tariff headwinds, all of which are transient?

6.6x owner earnings for a business generating 58% gross margins with a 20-year track record of brand durability. The market is wrong.

Net debt of ~$1.1 billion ($1.23B debt minus $130M cash) against ~$700M operating cash flow puts net leverage at roughly 1.6x EBITDA. Management targets 1.0-1.5x and is actively deleveraging. The maturity schedule is manageable. No near-term refinancing risk. Balance sheet is not a concern.

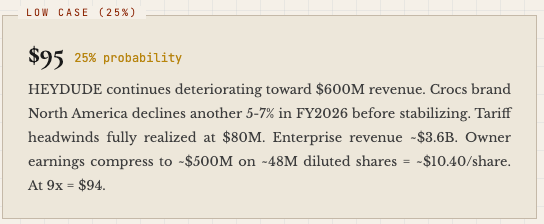

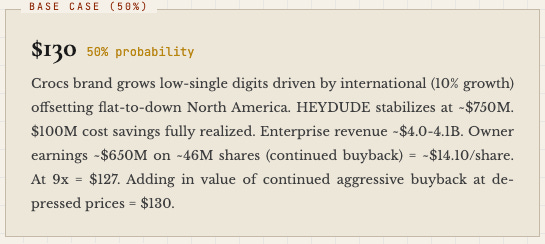

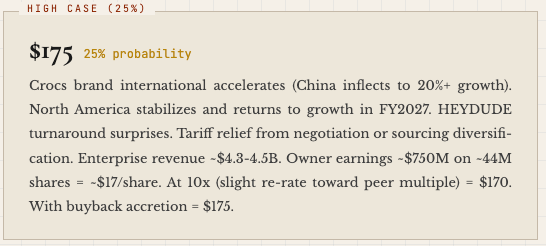

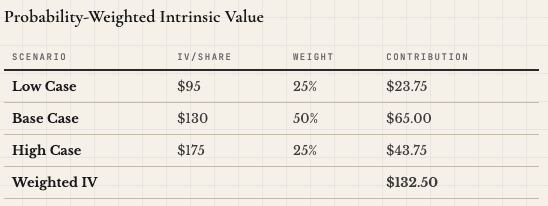

Valuation & Margin of Safety

I use three probability-weighted scenarios summing to 100%. Each scenario models a different trajectory for the core Crocs brand and the HEYDUDE drag. The market cap at $79.54 with ~50M shares is approximately $3.98 billion. Enterprise value (adding ~$1.1B net debt) is approximately $5.1 billion.

At $79.54, the stock trades at a 40% discount to probability-weighted intrinsic value. Even the low case ($95) offers 19% upside from the current price. The margin of safety is not in the assumptions. It is in the price.

Risks, Kill Switch & Scuttlebutt Actions

Primary Risks

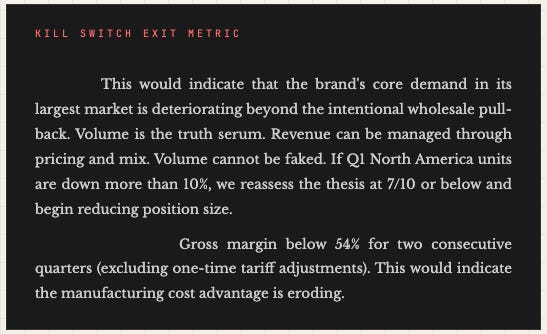

1. HEYDUDE total impairment. If HEYDUDE revenue declines below $500M and the brand requires goodwill writedown, GAAP earnings take a massive hit. This does not affect owner earnings but does affect sentiment and potentially management credibility. Probability: Low-Medium.

2. Tariff escalation. The $80M annualized headwind assumes current tariff levels. If tariffs on Vietnam-sourced goods increase materially, gross margins could compress below 55%. Probability: Medium. Mitigant: Crocs is already diversifying sourcing and the product’s price elasticity is lower than competitors (customers pay $50 for clogs regardless).

3. Brand fatigue. The existential risk that Crocs “goes away” culturally. This has been the bear thesis since 2008. Eighteen years later, the brand is stronger than it has ever been, generating $3+ billion in annual revenue. Probability: Very Low.

4. Rees departure. Andrew Rees has been the architect of the turnaround. If he departs without a credible succession plan, the thesis weakens. No current indication of departure. Probability: Low.

Scuttlebutt Actions

Visit 3+ Crocs retail locations and assess foot traffic, inventory levels, and promotional intensity relative to last year

Monitor Google Trends for “Crocs” brand search volume vs. “HEYDUDE” to assess relative brand momentum

Call or email 2+ wholesale channel partners (shoe retailers) and ask about Crocs sell-through rates and HEYDUDE markdown pressure

Review Vietnam trade policy developments and monitor any expansion of tariff scope on footwear

Track insider transactions weekly through SEC Form 4 filings, particularly any Rees or CFO Susan Healy selling

Monitor Jibbitz charm sales data if available (high-margin attach rate is a proxy for brand engagement)

Attend Q1 2026 earnings call (May 14) and specifically probe North America volume and gross margin guidance

Excellent. Thanks for writing and sharing.